Full-code strategy runtime

Run complete strategy lifecycles across start-up, universe selection, bar handling, insight generation, pipeline processing, and teardown.

AQE is a standalone open runtime for builders who want code-level control over strategy logic, integrations, backtesting, and live execution. AQS adds visualisation and operations around it, but AQE does not require AQS to run.

AQE is designed for builders who need the structure of a quant platform while keeping ownership of strategy logic, runtime choices, and execution infrastructure.

Run complete strategy lifecycles across start-up, universe selection, bar handling, insight generation, pipeline processing, and teardown.

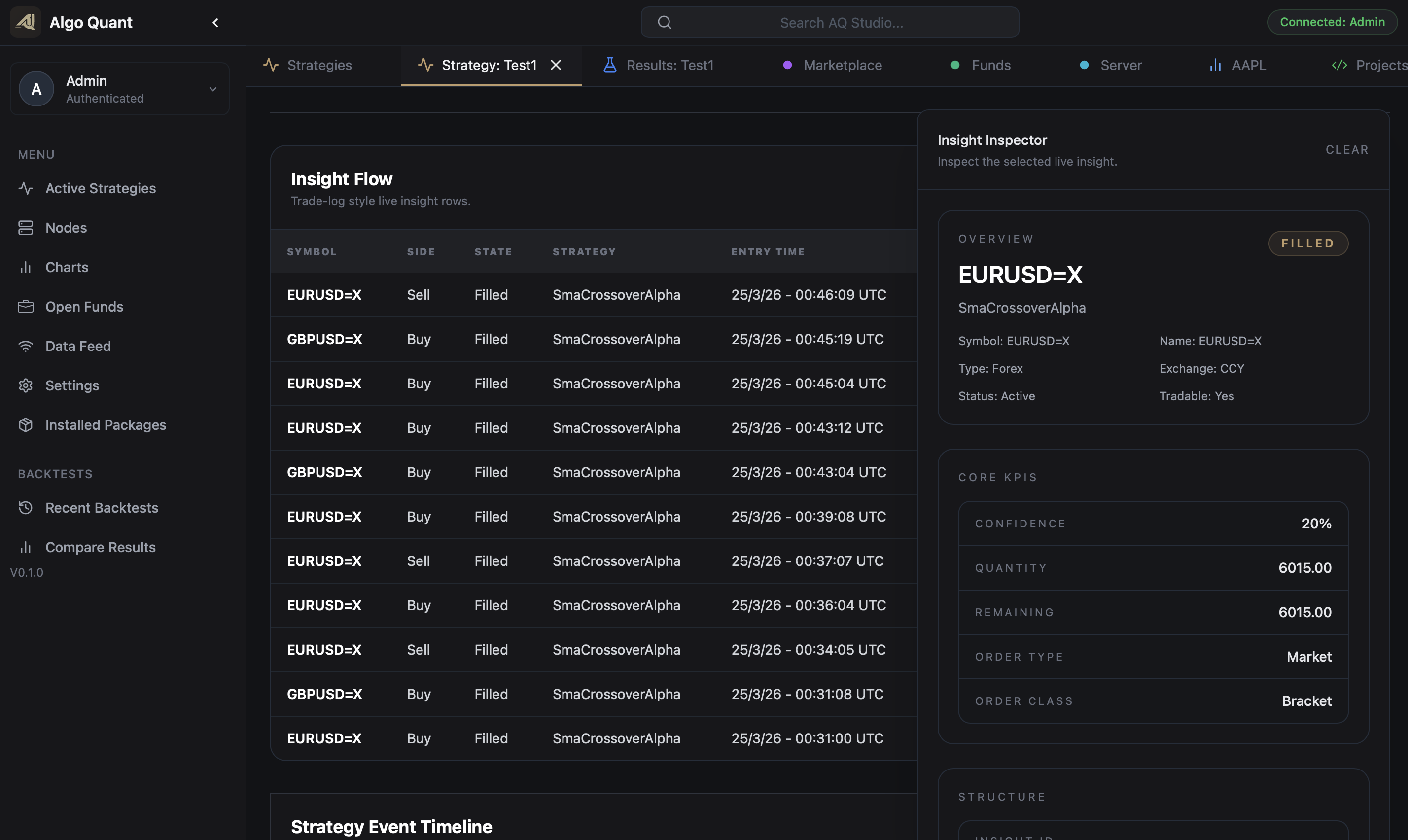

Represent trading intent as a first-class object with state history, order context, fills, closes, cancellations, and rejections.

Build against one engine-facing model while swapping execution, market-data, and infrastructure integrations behind the runtime.

AQE strategies can register additional bar event streams alongside the main strategy timeframe. Feature streams keep their own history frames, call into the same strategy lifecycle, and can optionally participate in signal generation when a strategy needs lower or higher timeframe confirmation.

The main strategy timeframe stays automatic, preserving the existing strategy surface for backtests and live runs.

Extra streams are stored separately with keys such as BTC:1m, TSLA:15m, or GBP/USD:1h so signal logic can read the right frame.

Strategies can inspect the current event context to decide which timeframe, symbol, and history frame should drive a calculation.

AQE keeps broker execution and market-data access behind engine traits, so the strategy code remains consistent while the runtime swaps datafeeds and broker integrations.

PaperBroker simulates orders, fills, closes, bracket legs, trailing stops, trade events, and account state for historical runs.

YahooFinanceDataFeed and configured MT5 datafeeds can provide historical bars for research and backtest market streams.

Mt5Broker and Mt5DataFeed connect AQE to MetaTrader 5 for live account state, order routing, quote updates, and bar streams.

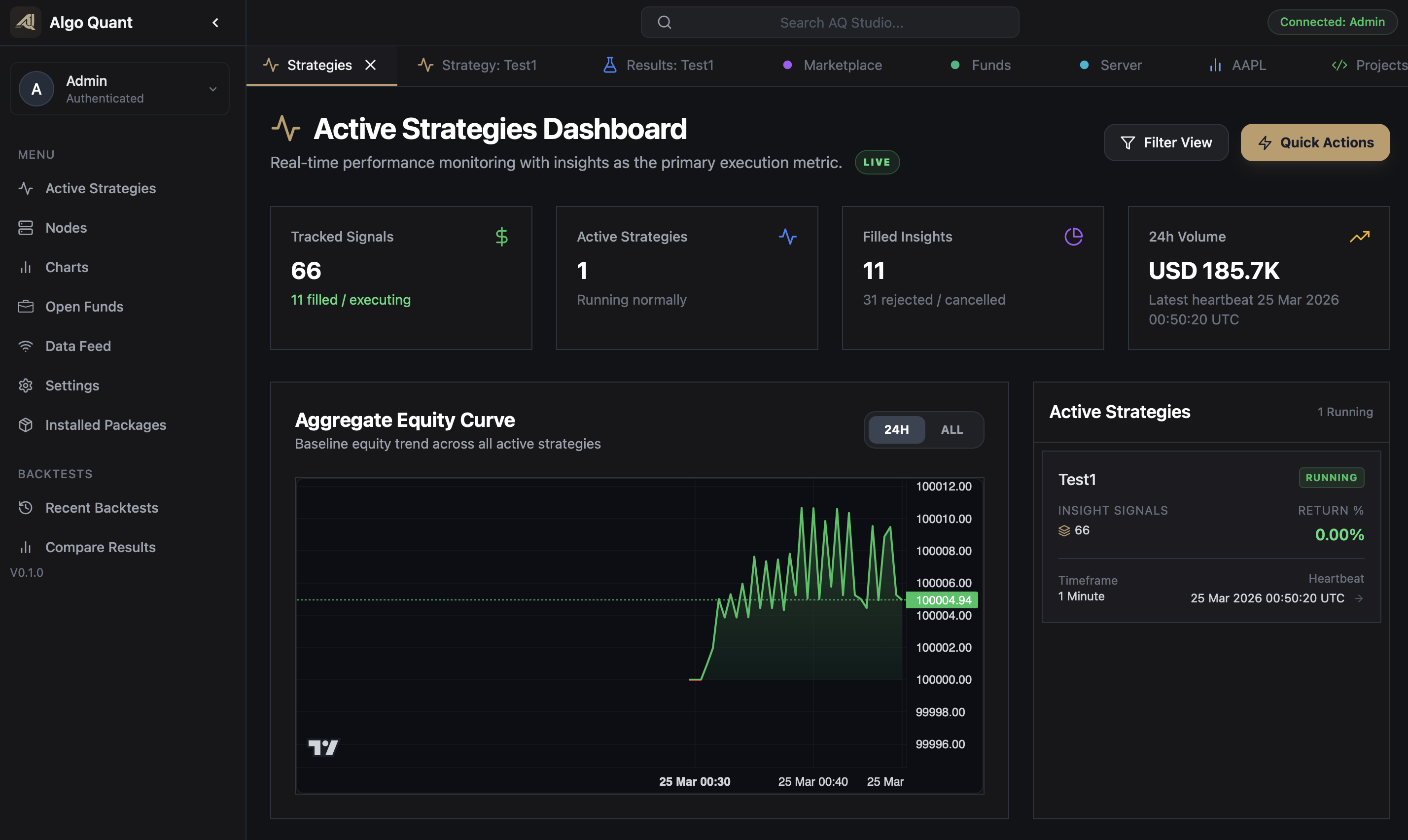

AQE can render a Ratatui terminal UI for backtests and live sessions, showing progress, metrics, active insights, nested strategy variables, watched state, logs, and AQS sync status from the running process.

Track processed market steps, event streams, logs, final metrics, and the saved result path without leaving the terminal.

Inspect active insights, AQS sync state, broker/datafeed status, universe, strategy variables, and watch paths during live runs.

For live strategies, the TUI requests teardown first so the engine can close cleanly before the interface exits.

The engine is organised around strategy state, insight state, broker events, and session-scoped records. That structure supports pro debugging, operational review, and future team workflows where decisions need a clear trail.

Use the same strategy surface for historical research and live sessions today, with backtest results persisted for review even without AQS.

Publish session state into AlgoQuant Studio when you want visual inspection, dashboards, and review workflows around the standalone engine.

Add broker, market-data, and infrastructure implementations behind the existing engine traits as the trading stack expands.

AlgoQuant Engine processes bars, generates insights, manages broker updates, and persists result data as its own runtime. AlgoQuant Studio is an optional interface for visual orchestration, inspection, and live operations.

AQE is suited to independent researchers, pro strategy developers, and trading teams that need a coherent runtime for research, customisation, live execution, SQLite-backed result review, and infrastructure integration.

We use essential cookies and storage for sign-in, account security, colour theme preferences, this notice, and required PostHog internal usage, session quality, and reliability metrics. We do not use advertising cookies.